There are certain necessary processes of life that stubbornly resist evolution: getting a marriage license, mailing a package, and, until now, applying for a mortgage. But there’s good news! At least one of them—getting a mortgage—has become, shall we say, painless. Seamless, even, if Quicken Loan’s new Rocket Mortgage app works as well asTech Crunch says it does.

Tech Crunch compares Rocket to TurboTax. That sounds about right to us. The app asks you to define your end goal—mortgage or refinance—and goes from there. Sure, your preferred lender may boast an online application, but there are still usually plenty of steps in the process that are definitely not digital or online. As any good, digital-first product does, Rocket Mortgage captures all your information once, repackages and distributes it for all necessary parties, and can verify bank balances—no need to submit bank statements!—and employment information in a real-time feed. Once all the information is submitted, Tech Crunch explains, “Several slider bars allow the mortgage-seeker to play with the fees and interest rate. If, say, the applicant wants to buy a better interest rate, slide the bar a bit and the data will adjust to show slightly higher closing costs, but a lower monthly payment and less interest that will be paid over the course of the loan.” The user can then lock a rate and send the application off for approval and purportedly receive an answer within minutes. My husband and I purchased a condo earlier this year. Our offer was accepted in late February, and we closed in early June. The three months in between were filled with endless printing/scanning/faxing/emailing of personal and financial information, much of which was duplicative. I have to wonder if I wouldn’t have maintained a little more of my sanity had something like Rocket Mortgage been around. The disadvantage of the app is that you won’t be shopping around for a loan from another lender; you can only tweak the details of Quicken Loan products. The company spent three years building the technology, and there’s a good chance other mortgage companies are working on competing products, but it could be quite some time before we see comparable apps. Stay tuned to your app store!

0 Comments

Sure, plenty of homes out there have been owned by celebrities at some point. But few boast the star-studded history of 2620 Benedict Canyon Dr. in Beverly Hills, CA—and its star status could shine even brighter now that it’s on the market for $6.99 million. “It’s interesting for a home to have so many owners with a strong Hollywood history,” notes listing agent Heather Bilyeu. The two-story home is “perched above the street” with “lots of foliage,” ensuring privacy. “You don’t see any other house, and no other house is looking at you,” she says. The home features hardwood flooring, an expanded and updated kitchen, vaulted and beamed ceilings, and a stone patio filled with trees. Beyond the home’s gorgeous features, many may be intrigued by its dynasty of famous owners. Curious to hear who among the Hollywood elite have inhabited these four walls? Check out this timeline below:  1976This mansion is built for William Asher, producer and director of iconic TV shows such as “The Dukes of Hazzard” and “Bewitched” (Asher was once married to Elizabeth Montgomery, the actress who played suburban sorceress Samantha Stephens). It was smaller than its current 5,076 square footage and looked a bit different, too. “It was probably a quaint, charming little farmhouse somewhere in the 2,500-square-foot range,” speculates Bilyeu. 1983From witches to … angels? Kate Jackson, who played one of the three original female detectives on “Charlie’s Angels,” bought the home from Asher and Montgomery. 1991Master saxophonist Kenny G bought the five-bedroom home—then expanded it to incorporate a recording studio where his instrument could perform those oh-so-sexy tunes (it now functions as a game room).  1998Seven-time Wimbledon winner Pete Sampras—perhaps the greatest American tennis player of all time—purchased the home this year. Naturally, he added a tennis court on the 1.66-acre estate. 2004Jon Peters—the Hollywood producer who brought us movies such as “Man of Steel” and 1989’s “Batman”—buys the home with his now ex-wife Mindy Peters, who remains the current owner. “Mindy recently finished a cosmetic remodel, updating it to a Hamptons-style restoration,” Bilyeu says.  So who’s next?The house has been on the market for a little over a week, and it might not be for sale much longer. Bilyeu just held a “very busy” open house with one celebrity coming back later to walk around—and he “walked it for quite some time,” she says.

Or maybe it will be Scott Disick, reality TV star and father to babies with Kourtney Kardashian. Disick was spotted checking out the property with Josh Altman, who’s Bilyeu’s fiancé, according to TMZ. The couple star on “Million Dollar Listing Los Angeles.” So if you’re in the market for a million-dollar mansion in the 90210, give Bilyeu a ring. After seeing this place, you might just have the moment you’ve been waiting for.  Homeowners aren’t usually thinking about their future tax bills when they embark on a remodeling project. But they’d be smart to at least give them a second thought. That’s because renovations can significantly raise a home’s value, which can increase the amount for which it is assessed. Assessed value is used to determine your property tax.

The improvements that would trigger a property’s reassessment vary by location. For example, adding a bathroom in Los Angeles will likely trigger reassessment; in Chicago, as long as the new bathroom is part of the home’s existing livable space footprint, it likely won’t, according to spokesmen from the assessor’s offices in Los Angeles and Cook counties. Home remodeling spending is forecast to rise in the coming year. The Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University recently projected that annual spending growth for home improvements would rise to 6.8% in the second quarter of 2016, up from 2.4% in the third quarter of this year. And as homeowners cram their extended families into their houses this holiday season, they may start to fantasize about projects they’d like to do in the coming year. When you embark on a project, the local assessor’s office will likely learn of it through building permits filed. But oftentimes you can ask in advance whether a particular improvement will increase your home’s assessed value. (In some places, they might even help you get a rough estimate of your new post-remodeling tax bill.) Here are examples of improvements that can increase your taxes: Additions and increasing living spaceAdding a new wing to a home will most likely increase your property taxes. But so will finishing space that you already have, such as an attic, garage or basement. “Anything that increases the square footage of the living space is likely to increase the value of the home, and therefore the assessed value,” said Tom Shaer, deputy assessor for communications with the Cook County Assessor’s Office. Your value would likely increase if, say, you finished the attic with walls and flooring, as well as heating, ventilation and air conditioning systems (HVAC), to create a couple of bedrooms and a bathroom, or if you finished the garage, creating a family room. It probably would also increase with a finished basement, though at a different rate than above grade areas of the home (unless a separate-entry apartment is created), Shaer said. Large renovationsAdding a bathroom is a common improvement that will trigger reassessment of a home, mainly because an “additional bathroom allows more people to live in the house,” therefore increasing its value, said Pete Sepp, president of the National Taxpayers Union, a pro-taxpayer lobbying group. But other substantial home alterations may also trigger reassessment in some places. In Los Angeles County, for example, adding a bedroom or fireplace could also make for a bump in property taxes, said Michael Kapp, public information officer for the Los Angeles County assessor’s office. Kitchen renovations are more of a gray area, Kapp said. “If they’re replacing countertops and not extending them, it would probably not [trigger a reassessment],” Kapp said. “If they add additional cabinets or move a wall, for example, that would trigger reassessment,” even if the square footage remains the same. Of course, it probably goes without saying, but if you’re gutting and renovating a rundown abandoned home, you can pretty much bet that your place will be reassessed, said Kelly Balensiefer, the assessor in Benton County, Ind. On the other hand, if an improvement serves to merely update the home, the value won’t likely change — and the assessed value will stay put. “We try to err on the side of the taxpayer,” only reassessing in the case of substantial improvements, Balensiefer said. Not-so-obvious improvementsIn some cases, adding a garden shed will trigger a reassessment, Sepp said. An in-ground pool or, perhaps, a very large deck could also equal a bump in your property tax bill, since they may be seen as adding value to the property, Balensiefer said. In Chicago, a screened-in porch won’t add value to the home; make it a four-seasons room with HVAC, and the assessed value will go up, Shaer said. Perhaps even less obvious are improvements made to the property, which have little to do with the house at all. For example, re-grading the lot to improve its drainage, if it was susceptible to flooding or sewer backup, might increase the assessed value, Sepp said.  If your Black Friday ritual involves rolling out of bed at 4 a.m., engaging in a 20-minute standoff over a parking spot, and standing in scary-long lines for doorbuster deals to put under the Christmas tree, consider this: What could possibly be a better gift than a new house? Black Friday and Cyber Monday aren’t just for fabulous deals on the Apple Watch and Beats by Dre. You can get a sweet break on houses, too! We sifted through our listings to find some gorgeous homes that have seen recent price cuts. And boy, are there some deals out there. Sure, some sellers knocked off only a few grand, but others cut their prices by hundreds of thousands of dollars! So put your PJs back on, get out the leftover turkey, and take a tour with us of some of America’s best deals—on real estate. 9360 N Lake Dr, Bayside, WI Was $699,900 in July Now: $549,900 This five-bedroom, Cape Cod beauty comes complete with a screened-in sleeping porch, five (five!) fireplaces, and original 1941 details. The home measures 5,173 square feet.  73 Union Ave, Saratoga Springs, NYWas $1,899,000 in April Now: $1,749,900 This charming turn-of-the-century estate is so enormous, it’s basically a two-fer. With nearly 10,000 square feet, the Victorian Queen Anne home boasts six bedrooms, six full bathrooms, two half-baths, an adjoining carriage house, and a wraparound porch. Bonus: It was all renovated just last year.  908A Toney School Rd, Toney, ALWas $824,900 in June Now: $799,000 Have the kids been bugging you for a pony for Christmas? How about giving them a whole horse farm? This 25-acre equestrian property comes with a 10-stall barn, riding arena, and even a natural spring/pond. It comes with a 4,679-square-foot house, including soaring ceilings and custom details. The $26,000 discount is not the biggest price chop we’ve seen, but anything more might be downright theft!  1611 Mokulua Dr, Kailua, HIWas $18,500,000 in April Now: $16,500,000 Even big spenders like a good deal, and here’s an amazing one. The owners of this fantasy home chopped the price this month by a cool $2 million. Once we figure out a way to pool our money and somehow come up with $16.5 million, we’re totally going to buy this place. Don’t worry—we’ll invite you over. With five bedrooms, a poolside pavilion, and a guest suite, there’s room to spare.  1118 Mallorca Dr, Bradenton, FLWas $369,000 in October Now: $350,000 Want some bang for your buck? This Florida gem touts a brand-new paint job throughout, crown molding, and even a new roof. The 2,468-square-foot, five-bedroom home is also a mere four miles from the beach. Talk about a bargain!  15285 Brunswick Dr, Shasta, CAWas $799,900 in March Now: $750,000 Stunning forest views set this 5,150-square-foot home apart from the pack. The five-bedroom home on nearly 8 acres boasts custom upgrades throughout and a setting perfect for entertaining—complete with a game room, “backyard retreat,” and swimming pool.  7925 E Cloud Rd, Tucson, AZWas $390,000 in June Now: $350,000 Beautiful desert living for $40,000 less? Yes, please! This updated masonry home touts a chef’s kitchen, a swimming pool, and a basketball court. It also comes with luminous sunset views that belong in an art gallery. We don’t know why somebody hasn’t grabbed this home yet, but we’re grateful for the discount!   Moving to a new place can bring a lot of fresh starts, but will it help wipe your debt slate clean?

Many commenters getting ready to relocate to another state have asked whether a judgment in their old one will still stand, once they have moved. Unfortunately, unlike a ratty old couch or all those terrible holiday sweaters your great aunt kept giving you for Christmas, old debts aren’t something you can really leave behind. In fact, “the United States Constitution requires the new state to give full faith and credit to the judgment issued by the first state,” says April Kuehnhoff, a staff attorney at the National Consumer Law Center. However, the creditor or debt collector will have some business to take care of before they can come knocking on your new door. “To reach assets in the new state, the creditor must apply to a court in the new state,” Kuehnhoff says. Most states follow what’s known as the Uniform Enforcement of Foreign Judgments Act when it comes to dealing with cases that cross state lines. The Act requires that creditors file an authenticated copy of the judgment with a court in the state where enforcement is sought and an affidavit establishing the names and last known addresses of the debtor and creditor. The court will then send notice of the filing to the debtor at the address the creditor provided. In places that don’t follow the Act (California, Massachusetts, Puerto Rico and Vermont), “the process of domesticating a judgment … may be more complicated,” Kuehnhoff says. But, in either case, you are ultimately legally responsible for the debt, given the original court ruling against you. And your move won’t do anything to stop a judgment from appearing on your credit report and damaging your credit score while you wait for new paperwork to be filed. (You can see how your debts many be affecting your credit by pulling your credit scores for free every month on Credit.com.) What can I do?Creditors or collectors often treat judgments as tools to get a debtor to repay on a debt, so, whether you’ve relocated of not, there’s still a chance you can avoid a property lien or wage garnishment. “Contact the creditor to try to work out a payment plan or try to negotiate for a lower amount [than what the judgement requires you to pay],” Kuehnhoff says. You may also want to consult a consumer law attorney in your new hometown to see if the move entitles you to some extra protections, regarding how a creditor can collect what you owe. These laws vary state by state and the creditor or debt collector behind the judgment will be required to honor the rules in your new hometown.  The chill will be here before you know it—or, depending on where you’re reading this, it’s already arrived with a scary vengeance. Now you have three options: Crank up the thermostat, up your layering game (and risk looking like the Michelin man), or search for other types of home heating products to keep you and the family toasty. Here’s the good news: There’s a slew of products that can warm your home in an array of astonishing ways, from heated rugs to countertops to driveways (no more shoveling snow!). Here’s a sampling of the innovative options. Heating panels  Radiators and vented systems work perfectly well throughout the house, but add a few radiant heating panels to your room of choice to fire up the cozy factor. Starting at $600; warmlyyours.com. Heated driveway  You might love a fresh snowfall a little more (instead of cursing it) if you don’t have to shovel it. You can increase safety and eliminate snow and ice by installing a heated driveway. Around $2,500 plus installation; heatizon.com. Heated rug pads  A heated rug sounds pretty appealing, no? The plug-in pad slips under a standard area rug. We have a feeling the kids (and pets) will be flocking to this one. Starting at $150;cozywinters.com. Heated countertops  The cool touch of granite is fabulous in the summer, but it’s not so great when you’re trying to make coffee on a chilly winter morning. The solution: heated countertops. Installable and stick-on are available. Starting at $750; feelswarm.com. Heated towel rack  You can banish après-shower cold shocks with this toasty towel rack, one of the products that helped kick off the whole heated gear trend a few years back. $160;wayfair.com. Heated mattress cover  Ten heat settings and dual control means everyone will be snug on this sherpa mattress cover. Starting at $65; target.com. Boot heater  Can’t bear the thought of slipping your little piggies into wet, cold boots for another schlep outside? Avoid the torture with a space-saving boot dryer. $35; cozywinters.com. Heated slippers  These heated indoor-outdoor slippers work as shoes, too, depending on your definition of footwear and, um, style. $125; brookstone.com. Heated toilet seat  Let’s be honest: This heated toilet seat (with night light!) is quietly appealing. We’ll leave it at that. $122; homedepot.com.

Whether you can afford to buy a home largely boils down to two things: where you live and how much money you earn. Wondering if your paycheck passes muster in your preferred neighborhood? New analysis from mortgage website HSH.com has pinpointed the minimum salary you’d need to purchase a home in various cities—and wow, the range just goes to show just how much pricier (and cheaper) certain places are than others!

To come to these latest figures, HSH.com examined the National Association of Realtors®’ 2015 third-quarter median home prices in 27 metropolitan areas, along with HSH.com’s 2015 third-quarter average interest rates for a 30-year, fixed-rate mortgage. From there, it tallied up how much it would cost to afford the monthly payments on an average home—principal, interest, taxes, and insurance—if you put down 20%. Oh, and you would still have money to eat and otherwise make ends meet. While you can check out HSH.com for a full rundown of the base salary required in all 27 cities, here’s a glance at a dozen worth noting, from least to most expensive. Orlando, FLMedian home price: $201,200 Monthly mortgage payment: $1,103 Salary needed: $47,500 Minneapolis, MNMedian home price: $288,700 Monthly mortgage payment: $1,199 Salary needed: $51,500 Philadelphia, PAMedian home price: $234,700 Monthly mortgage payment: $1,291 Salary needed: $55,500 Chicago, ILMedian home price: $229,300 Monthly mortgage payment: $1,432 Salary needed: $61,500 Portland, ORMedian home price: $319,300 Monthly mortgage payment: $1,551 Salary needed: $66,500 Denver, COMedian home price: $353,000 Monthly mortgage payment: $1,608 Salary needed: $70,000 Seattle, WAMedian home price: $386,300 Monthly mortgage payment: $1,849 Salary needed: $79,000 Washington, DCMedian home price: $388,600 Monthly mortgage payment: $1,910 Salary needed: $82,000 New York City, NYMedian home price: $410,500 Monthly mortgage payment: $2,134 Salary needed: $91,500 Boston, MAMedian home price: $449,000 Monthly mortgage payment: $2,165 Salary needed: $93,000 Los Angeles, CAMedian home price: $506,800 Monthly mortgage payment: $2,322 Salary needed: $99,500 San Francisco, CAMedian home price: $809,400 Monthly mortgage payment: $3,573 Salary needed: $153,000  Yes, my husband and I did it: We bought a fixer-upper, and it nearly did us in. It wasBrooklyn, NY, in 2008. I remember walking to the place for the first time and seeing the back seat of a van on cinder blocks being used as a couch—and quickly looked past that eyesore. This could be a great space once it was renovated, I thought. The light was abundant, the space ample and flexible, and its Park Slope neighborhood was about to bloom. Six months into the renovations, our contractor told us: “In hindsight, we should have knocked this down and started from scratch. It would have been cheaper.” Ah, blessed hindsight. We wanted to keep you from getting sucked into a money pit of your own. For expert advice, we turned to Cathy Baumbusch, a Realtor® in Washington, DC, who told ushow to master the art of buying a fixer-upper. 1. Know that some flaws can be fixedFixer-uppers generally fall into two categories: total wreck and ugly house.

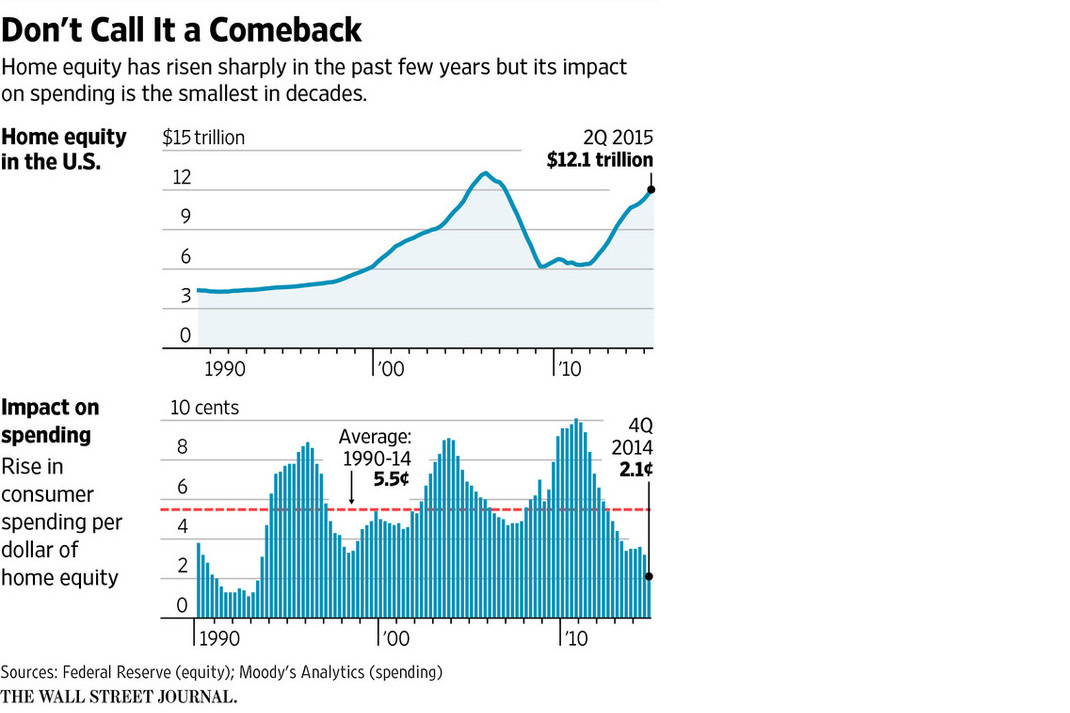

“An ugly house is not architecturally appealing: Its paint is chipping away, the yard is unkempt, inside it may smell bad,” says Baumbusch. In short, everything about it needs freshening up. But if these are the kinds of flaws you’re dealing with, take heart: They’re merely cosmetic, and they’re easy to fix. Painting is the easiest task that you can do yourself. Just don’t cut corners—buy all the right equipment (use the tape!) and paint correctly, with the right number of coats. It’s extra work, but it pays off in the end. Even if you hire a painter, it won’t cost as much as redoing the bathroom. You could also refinish the floors yourself, although it involves renting a machine. 2. Then again, other flaws cost a bundleOn the other hand, some blemishes may initially slide under your radar—but eventually make a big impression on your wallet. “Problems with the foundation, structure, roofing, and siding can be expensive to fix,” says Baumbusch—as can major replacements with sewage, septic, and heating, ventilating, and air-conditioning systems. Replacing decks and driveways can also be costly. Sometimes environmental problems such as a wet basement or mold can be mitigated, but treatments are not always successful. In some houses, it can just be impossible to solve a bad mold problem. “I once viewed a property for sale where the mold was so bad, it was difficult to breathe,” says Baumbusch. “It was everywhere, and the property management company was doing nothing to stop it. That home would probably be better off completely gutted or razed altogether.” 3. Ballpark your renovation costsHire a structural engineer to evaluate the home before you buy—but before you even get there, do your research. There are a lot of repair estimators out there, so ask your friends and co-workers if they’ve done repairs lately and could tell you how much they cost. That way, you can quickly ascertain whether the repairs would fall within your budget. Draw up a reference sheet for renovation costs such as roof, foundation, HVAC, and windows. This will help you to determine a viable offer price. 4. Ask for a discount—gentlyNow on to the real upside of buying a fixer-upper: major savings! These houses can go for as little as 60% to 80% of the original asking price, says Baumbusch. This is especially true if the home has been sitting on the market for a while, or if you’re able to offer cash upfront. Of course, even if you and everyone within eyeball range know that this house is in shambles, that doesn’t mean the sellers know that, or want to hear it. To avoid insulting them, start out by saying you love their home, but you (or your engineer, inspector, or friend) have noticed some issues that will take time and money to fix. Then subtract that sum from their asking price, and you don’t have to stop there. If the renovations will keep you from living (or living comfortably) in your home, it’s also customary to tack on an extra fee for what Realtors call “the hassle factor,” which can be estimated by the amount of time and money you’d spend living elsewhere while the renovations happen. The bottom line: The more you break down your expenses, the more sense your offer will make to the sellers, who will hopefully play ball. 5. Get the right kind of loanA home requiring major renovations can qualify for a special type of financing called a renovation loan. And there are different types: A 203(k) loan, recently rising in popularity, is insured by the Federal Housing Administration. Since these loans are backed by the government, lenders are fine accepting lower interest rates than what would be required by your typical home renovation loan; they’re also open to people with less-than-stellar credit. The downside? There’s a limit to how much you can borrow (anywhere from $271,000 to $729,750, depending on the price of property in your area). Be sure to explore all your options with your Realtor or other qualified experts. In the case of our Brooklyn home, we transformed a disheveled hovel into a beautiful home. It took a very long time and a lot of money. It just might have been nice to know what we were actually getting into to try to avoid the panic that came with every change order. So, if you’re thinking about tackling a fixer-upper, trust me—it helps to know what you’re in for first.  American homeowners are finally digging out of the hole created by the housing crisis. But their housing wealth is playing a much smaller role in the overall economy than it did before the downturn. Home equity has roughly doubled to $12.1 trillion since house prices hit bottom in 2011, according to the Federal Reserve. As a result, a key gauge of housing wealth—homeowners’ equity as a share of real-estate values—is nearing the point seen a decade ago, before the downturn. Such a level once would have offered a double-barreled boost to the economy by providing owners with more money to tap and making them feel more flush and likely to spend. But today, that newfound wealth has had little effect on behavior. While the traditional ways Americans tap their home equity—home-equity loans, lines of credit and cash-out refinances—are higher than last year, they are still depressed. In the first half of the year, owners borrowed $43.5 billion against their homes with home-equity loans and lines of credit, according to trade publication Inside Mortgage Finance. That was 45% higher than in the first half of 2014, but scarcely a quarter of the amount seen when equity was last as high in 2007. Meanwhile, cash-out refinances, which let homeowners take out a new mortgage and tap some of the home’s value at the same time, were up 48% in the three months ended in August from the year-earlier period, according to Black Knight Financial Services.But they remain below the level seen in the summer of 2013. The average cash-out refinance in the three months ended in August left the borrower with mortgage debt of about 68% of the home’s value—not a risky level by any stretch. Home equity’s effect on consumer spending is at its lowest ebb since the early 1990s, according to Moody’s Analytics. The research firm estimates that every $1 rise in home equity in the fourth quarter of 2014 would translate to about two cents of extra consumer spending over the next 1 to 1½ years. That was a third of the impact home equity had before the bust, Moody’s said.  The impact is more muted now despite the fact that home equity per homeowner has roughly doubled. At the end of the second quarter, the figure was about $156,700, up from $81,100 in the second quarter of 2011, according to Moody’s Analytics chief economist Mark Zandi. Though the homeownership rate has fallen, the total number of households has increased, meaning the number of households that own hasn’t changed much since the housing bubble burst in 2006, Mr. Zandi said.

Why aren’t homeowners feeling flush again? For one thing, since rising home prices over the past few years largely have made up for ground lost during the recession, many owners might not even realize they have equity to tap. The percentage of homeowners who were underwater, or owing more on their mortgage than the home’s value, dropped to 8.7% by mid-2015 from 21% at the end of 2011, according to CoreLogic. Yet the percentage of homeowners who thought they were underwater fell by merely one percentage point to 27%, according to housing-finance company Fannie Mae. The bust looms large and home equity is seen as more fleeting than it used to be, said Fannie Mae chief economist Doug Duncan. “Consumers are definitely more conservative financially than they were 10 years ago. They’ve seen that house prices can be volatile,” Mr. Duncan said. Mortgage lenders also aren’t giving owners access to as much equity as they used to. While it was common during the boom to see loans that took out 100% or even more of a home’s value, now few will let an owner take out more than 80%. Finally, other kinds of loans are cheaper, removing one incentive to tap home equity. Six years ago, for example, the average five-year new-car loan had an interest rate of 6.83%, versus 5.56% for a $30,000 home-equity credit line. But in the week ended Nov. 11, the average interest rate for a five-year new-car loan was 4.3%, according to Bankrate.com, versus 4.74% for the HELOC. Home equity as a share of real-estate values at the end of the second quarter was 56%, according to the Federal Reserve, not quite back to the level of 60% seen in the boom. That means Americans’ mortgage debt is still elevated relative to home values, which could be another factor affecting the decision of whether or not to cash out equity. Could home equity start to flex its muscle sometime soon? Some economists think it might. One reason: In many metro areas, home prices have overtaken or are about to overtake their boom-era peak. About 38% of metro areas had prices above their pre-2009 peak at the end of the third quarter, up from a 30% level last year, according to Moody’s Analytics and CoreLogic. A further 13% of metros are within 5% of their prebust peak. That’s important, because it means new home equity is being created rather than merely making up for lost ground. It also means fewer homeowners are underwater, freeing them up for a home sale and potential move-up purchase while also making home improvements and renovations seem less like throwing good money after bad. “We’re at an inflection point,” Mr. Zandi said. “Since the crash, it’s all been about repairing homeowners’ equity but now that house prices are returning to prerecession levels, we will see homeowners’ equity driving consumer spending, home improvements and economic activity.”  If you manage to tear your eyes off Cookie and Lucious’ intense relationship, then you’ve probably drooled over the insanely cool set design on “Empire.” The homes featured on the so-bad-it’s-great Fox drama are as opulent and interesting as the hip-hop mogul hero/villain and his family members who inhabit them. Whether it’s Lucious Lyon’s (Terrence Howard) lavish mansion or Jamal’s (Jussie Smollett) sleek townhouse, these interiors were artfully put together by veteran set decorator Caroline Perzan. We talked to Perzan about the design secrets hiding within these gorgeous often-gated homes—and how you can apply them to your own, presumably less glamorous, life. Secret No. 1: Combine old with new, sometimes in the same piece“In Los Angeles, it’s easy to decorate a show, because there are so many prop houses. But outside Los Angeles [the show is set in NYC but shot in Chicago], it becomes more of a challenge. I think it’s more fun in a way, because you get to be far more creative. I was buying a mid-vintage couch in an antiques shop and decided to update it to a more high-end Mid-Century Modern look. By the time I am done with it, I will make it look like it’s worth $20,000. And it will be a unique piece. That’s much more interesting than going to a prop house for a couch. And in real life it’s a more interesting approach, too.”  Secret No. 2: Decorate a room around a special item“The grand piano in Lucious’ office is designed by Warren Shadd, the only African-American piano manufacturer in the U.S. He is a lovely man who wrote me a letter introducing himself to me. Now, I get a lot of letters, but I thought this was really cool; the range of his pianos—baby, grand, upright—were really amazing. He came on his own dime to us, because he was passionate about the show and felt so strongly that the pianos should be a part of what we were doing. I would never have been able to afford them! Terrence has them tuned up to his specifications.”  Secret No. 3: Determine what art you love, and use it as a decorating motif“From the very beginning of the series, artwork has been a really big deal to Lee Daniels, ‘Empire’s’ co-creator. He loves contemporary African-American artwork, which is why the main character’s mansion is filled with it. He’s one of the few directors I’ve worked with who often starts a shot focusing first on the piece of art before bringing on the actor. I present some pieces to Lee, and then I figure out what room they should be in. I have more art on this show than I have had with any previous project I have ever worked! Not everyone has to spend what we spend on artwork, but figuring out what you love and decorating around it can add a lot to any room. “We have artwork in the mansion from well-known artists such asKehinde Wiley, Walter Lobyn Hamilton, and Mickalene Thomas, but Lee wanted to showcase up-and-coming artists, too. For the second season, to freshen things up a bit, Lee asked me to start checking out several art schools, and I have spent a tremendous amount of time getting to know several of the artists we have used on the show. “One example is a guy we found right out of art school, Jon Moody. One of his big mural pieces is in Jamal’s penthouse and has been featured quite a bit. Lee got so excited about Moody’s work and looks forward to making him famous! There’s no way an artist like Moody would ever have received this type of exposure if it weren’t for Lee.”  Secret No. 4: Be realistic about what you can and can’t have“The actors on the show try to take stuff home all the time. There is so much cool stuff on the set.Take those gold and platinum ‘Empire’ record albums in Lucious’ office. I have to say, ‘No! You can’t take them!'” ———Secret No. 5: Display your creations“Not only is Terrence a great actor and musician, he is also an incredible sculptor, too. He creates these incredible acrylic, three-dimensional sculptures. We would love to see them on the set, but of course, he hasn’t time to really work on them!”  |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

February 2016

Categories |

RSS Feed

RSS Feed